1. Introduzione

1.1 Scopo della ricerca

Questo rapporto mira ad analizzare e prevedere il mercato globale dei pannelli di visualizzazione dei telefoni cellulari, in particolare schermo LCD (display a cristalli liquidi) E OLED (diodo organico a emissione di luce) - oltre il Prossimo 20 anni (2025–2045). Fornisce informazioni dettagliate sulle tendenze delle spedizioni, crescita dei ricavi, dinamiche competitive, cambiamenti tecnologici, e rischi, supportare il processo decisionale strategico dei produttori, OEM, investitori, e politici.

1.2 Ambito: LCD mobile vs. OLED

Ci concentriamo su solo display dello smartphone, esclusi altri tipi come i televisori, monitor, o display automobilistici. La nostra analisi mette a confronto OLED rigidi e flessibili, diverse varianti LCD, e prevede quote di mercato a lungo termine, evoluzione tecnologica, e dinamiche regionali.

1.3 Metodologia e fonti dei dati

La nostra previsione è basata su:

- Dati storici e cifre di spedizione da Omdia (per esempio., Lo riferisce Omdia 2024, Spedizioni AMOLED raggiunte 784 milioni di unità, superando le spedizioni di TFT-LCD). Omdia+1

- Visualizza l'andamento dei ricavi (per esempio., SID Visualizzazione previsione settimanale: I ricavi degli OLED $46 B dentro 2024, schermo LCD $83 B). Visualizza Giornaliero+1

- Ricerca di settore da fonti del mercato cinese (per esempio., Proiezioni del mercato OLED cinese). Rete di notizie su Internet in Cina

- Proiezioni dei rapporti di mercato (Il mercato dei display per smartphone di MRFR da 2022 A 2032). futuro delle ricerche di mercato

- Ulteriori dati da annunci aziendali (per esempio., I commenti di Universal Display Corp che citano i dati di Omdia). cane con rapporto finanziario

2. Tecnologia di visualizzazione degli smartphone: Una panoramica

2.1 Che cos'è l'LCD?

schermo LCD (Display a cristalli liquidi) è una tecnologia di visualizzazione matura che utilizza una retroilluminazione che brilla attraverso cristalli liquidi per creare immagini. Ne esistono di vari tipi (TFT, IPS, ecc.), ma fanno tutti affidamento su una fonte di luce separata.

2.2 Cos'è l'OLED?

OLED (DIODO EMITTANO DI LUCE ORGANICA) i pannelli emettono luce propria: ogni pixel è auto-luminoso. Ciò consente neri più profondi, contrasto più elevato, e progetti potenzialmente più efficienti dal punto di vista energetico quando parti dello schermo sono scure.

2.3 Differenze chiave: Energia, Flessibilità, Costo

- Energia: L'OLED può disattivare i singoli pixel, ottenendo in alcuni casi una maggiore efficienza energetica.

- Flessibilità: I pannelli OLED possono essere resi flessibili, abilitando i telefoni pieghevoli.

- Costo: Storicamente, Gli OLED sono più costosi per unità rispetto agli LCD, soprattutto per le versioni flessibili o di fascia alta.

3. Contesto storico ed evoluzione del mercato

3.1 Prima epoca: Dominanza dell'LCD

All'inizio degli anni 2010, L'LCD era la tecnologia dominante negli smartphone a causa del suo costo inferiore e della produzione matura. La maggior parte dei dispositivi tradizionali utilizzava TFT-LCD o IPS LCD.

3.2 Ascesa degli OLED negli smartphone

Negli ultimi dieci anni, L'OLED si è gradualmente infiltrato negli smartphone di fascia alta. I vantaggi del contrasto, fattore di forma, e consumo di energia (in modalità oscura) lo rendeva attraente. I telefoni pieghevoli hanno accelerato l’adozione degli OLED flessibili.

3.3 Punti chiave di flesso

- Ingresso degli OLED flessibili nei pieghevoli

- Riduzione dei costi attraverso la produzione di massa

- Investimenti strategici da parte dei grandi produttori di pannelli (per esempio., Boe, SAMSUNG, Lg)

- Transizione dei principali OEM agli OLED per le linee premium

4. Stato attuale del mercato (2024–2025)

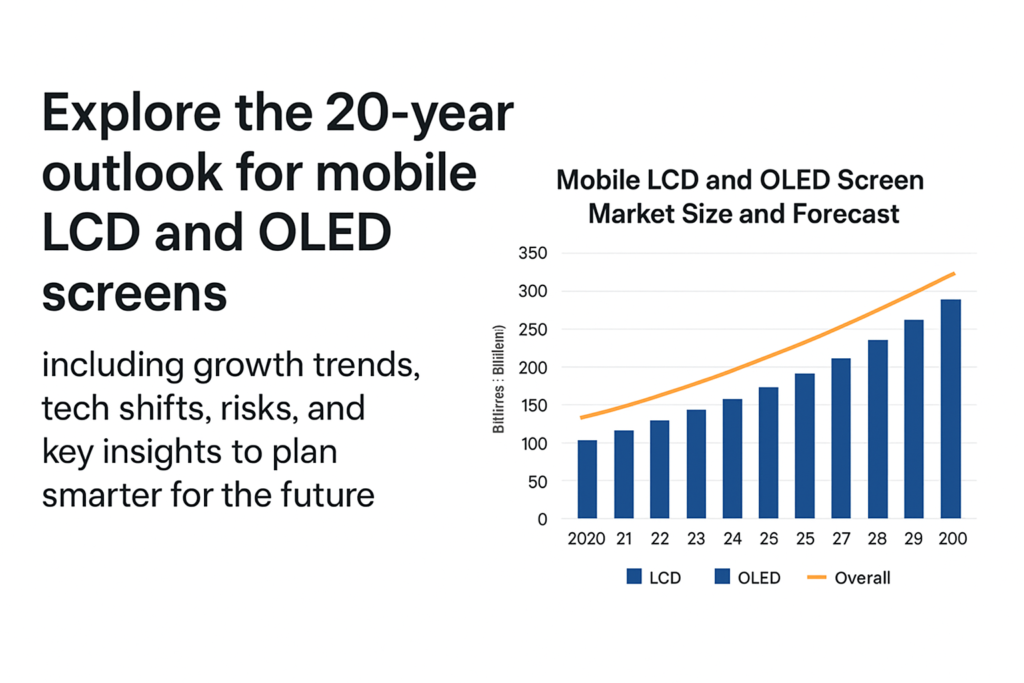

4.1 Dati di spedizione: OLED vs LCD (Unità)

- Secondo Omdia, In 2024, Spedizioni AMOLED raggiunto 784 milioni di unità, Mentre Spedizioni TFT-LCD sceso a 761 milioni di unità. Omdia

- Questo ha segnato il prima volta Le spedizioni di OLED hanno superato quelle di TFT-LCD negli smartphone. Omdia

4.2 Panorama delle entrate per tecnologia

- Basato sulla settimana di visualizzazione SID 2025 previsione, visualizzare i ricavi in 2024 erano all'incirca: OLED: $46 miliardi, schermo LCD: $83 miliardi. Visualizza ogni giorno

- Secondo il contrappunto in un'analisi cinese tradotta, Raggiunto il fatturato globale dei display OLED Dollaro statunitense 46 B In 2024. Fortuna orientale

- Omdia progetta OLED (AMOLED) ricavi da raggiungere $53 B nell'intero anno (previsione futura). Mondo mobile in diretta

4.3 Dinamiche regionali e attori chiave

- Cina è una forza importante: Produttori cinesi di OLED (Boe, Tianma, Visionox, ecc.) stanno crescendo in modo aggressivo. Omdia+1

- Corea (Schermo Samsung, Lg) continua a svolgere un ruolo di primo piano, soprattutto negli OLED flessibili.

- Secondo un rapporto sul mercato cinese, Si prevede che la penetrazione degli OLED flessibili in Cina aumenterà notevolmente; anche le tecnologie trasparenti/flessibili potrebbero espandersi. Rete di notizie su Internet in Cina

5. Driver per la crescita degli OLED

5.1 Costi di produzione in calo

- Con l'aumento della capacità della fabbrica OLED (soprattutto in Cina), il costo unitario diminuisce.

- La dimensione cinese dei produttori OLED flessibili e i prezzi competitivi hanno spinto più OEM a passare ai telefoni OLED di fascia media. Omdia

5.2 Flessibile / Tendenza degli smartphone pieghevoli

- L’ascesa dei telefoni pieghevoli alimenta la domanda di OLED flessibili.

- Secondo i rapporti dell’industria cinese, I fattori di forma pieghevoli sono uno dei principali motori della futura adozione degli OLED. Rete di notizie su Internet in Cina

5.3 Efficienza energetica & Esperienza di visualizzazione

- La capacità dell’OLED di spegnere i pixel offre un risparmio energetico, in particolare nelle modalità dell'interfaccia utente oscura.

- Gli utenti richiedono sempre più immagini più ricche, frequenze di aggiornamento elevate, e fattori di forma flessibili.

5.4 Innovazione nei materiali e nei Fab

- Nuovi processi come OLED stampato a getto d'inchiostro e la deposizione economicamente vantaggiosa stanno migliorando la resa e riducendo i costi.

- Gen-8.6 e altri fab avanzati sono in fase di costruzione per aumentare la produzione. Omdia

6. Sfide per l'adozione degli OLED

6.1 Pressioni sui costi di produzione

Produzione OLED (particolarmente flessibile) rimane più complesso e costoso dell'LCD. Il ridimensionamento richiede fabbriche ad alta intensità di capitale.

6.2 Concorrenza delle tecnologie emergenti

- MicroLED: Anche se ancora emergente, Il micro-LED rappresenta una potenziale minaccia a lungo termine.

- OLED QD: Le tecnologie combinate possono competere nei segmenti premium.

6.3 Rischi della catena di fornitura

Materie prime (composti organici, materiali di incapsulamento) e le attrezzature specializzate possono ostacolare la produzione.

6.4 Rischio di burn-in & Longevità

I pannelli OLED possono subire fenomeni di burn-in in determinate condizioni, sollevando preoccupazioni sull'affidabilità a lungo termine per alcuni utenti.

7. Il ruolo degli LCD nel futuro

7.1 Perché il display LCD rimane rilevante

- Produzione a basso costo

- Capacità di grandi volumi già esistente

- Filiera più semplice e più stabile

7.2 Basso costo / Segmento smartphone economici

Per telefoni entry-level e di fascia medio-bassa, Il display LCD potrebbe rimanere dominante a causa del suo vantaggio in termini di costi.

7.3 LCD Production Capacity Trends

Some LCD fabs are being repurposed, but many remain active for mobile display production.

7.4 Regionally Differentiated Demand

In markets where cost sensitivity is high (emerging markets), LCD will likely still serve a large portion of demand.

8. Market Size Forecast (2025–2045)

8.1 Base-case Scenario Assumptions

- Continued OLED adoption, particolarmente flessibile

- Moderate decline in LCD units but stable for budget segment

- No sudden disruption from Micro-LED before 2035

8.2 OLED Shipment Forecast

- OLED (AMOLED) shipments: growing from ~0.78 B in 2024, to over 1.2–1.4B units annually by the early 2030s (projected estimate based on trend)

- Revenue growth: from ~$46B in 2024 to potentially ~$70B+ in peak years (assuming ASPs stabilize or slightly drop but volume increases)

8.3 LCD Shipment Forecast

- LCD shipments may decline in absolute units — e.g., da 761 M in 2024, gradually to perhaps 400–600 M negli anni successivi mentre l'OLED riempie i segmenti medio-alti

- Reddito: il calo riflette sia il calo delle unità sia la pressione sui prezzi; ma rappresenta ancora una parte significativa del mercato totale dei display mobili a causa del volume dei dispositivi di livello inferiore.

8.4 Condivisione di OLED e LCD nel tempo

- Di 2030, OLED potrebbe catturare 60–70%+ del mercato dei display per smartphone per unità (soprattutto perché il flessibile diventa più comune)

- Di 2040, è possibile che vediamo OLED essere dominante (>70%) a meno che una nuova perturbazione non acceleri.

9. Tendenze tecnologiche & Innovazioni

9.1 OLED flessibile e pieghevole

- I telefoni pieghevoli continueranno a guidare la domanda di OLED flessibili.

- Altri OEM potrebbero lanciare dispositivi arrotolabili o estensibili, crescente domanda di pannelli flessibili.

9.2 LTPO, OLED tandem, Stampa a getto d'inchiostro

- LTPO (Ossido policristallino a bassa temperatura) i backplane consentono frequenze di aggiornamento variabili e risparmio energetico.

- OLED tandem impila gli strati per prolungare la durata e ridurre la potenza.

- OLED stampato a getto d'inchiostro può potenzialmente ridurre i costi di produzione e aumentare la resa.

9.3 Tecnologie ibride

- OLED QD (punto quantico + OLED) potrebbe rivolgersi ai mercati premium.

- MicroLED: pur essendo ancora nascente, crescita a medio termine (post-2030) potrebbe sfidare l’OLED in alcuni segmenti.

9.4 Sostenibilità & Efficienza energetica

- Il risparmio energetico degli OLED nelle UI scure contribuisce all'efficienza energetica.

- I produttori potrebbero investire di più in materiali ecologici e nel riciclaggio.

10. Previsioni del mercato regionale

10.1 Cina

- Forte aumento della capacità OLED.

- Produzione e adozione massiccia di smartphone a livello nazionale.

- L’OLED flessibile è già stato scalato dai produttori cinesi.

10.2 Corea del Sud

- Sede di Samsung Display e LG, continua leadership nell'OLED flessibile di fascia alta.

- Probabilmente rimarrà un fattore chiave nell’innovazione.

10.3 Europa & America del Nord

- Segmenti di dispositivi premium.

- Domanda stabile, ma la sensibilità ai costi potrebbe rallentare la piena penetrazione degli OLED nella fascia media.

10.4 Mercati emergenti (India, Sud -est asiatico)

- Sensibile al prezzo: Il display LCD potrebbe continuare ad essere forte qui.

- Ma man mano che i costi degli OLED diminuiscono, Gli OLED di fascia media potrebbero diventare mainstream.

11. Panorama competitivo & Giocatori chiave

11.1 Principali produttori di pannelli OLED

- Schermo Samsung: forte nell'OLED flessibile e premium.

- Schermo LG: OLED, flessibile, ma più limitato nei piccoli cellulari.

- Boe / Visionox / Tianma (Cina): crescendo rapidamente, competitivo in termini di costi.

11.2 Produttori di pannelli LCD & La loro strategia

- Alcuni produttori di LCD stanno ridimensionando; altri potrebbero orientarsi verso LCD di nicchia o specializzati.

- I produttori di LCD tradizionali devono decidere se investire negli OLED o semplificarli.

11.3 Nuovi partecipanti / Giocatori dirompenti

- Produttori emergenti di micro-LED.

- Startup che lavorano su processi OLED di prossima generazione (per esempio., getto d'inchiostro, tandem).

12. Rischi e incertezze

12.1 Rischi macroeconomici

- Recessioni, inflazione, Gli shock della catena di approvvigionamento potrebbero rallentare la domanda di smartphone.

- L’intensità di capitale delle nuove fabbriche è elevata: rischio se la domanda rallenta.

12.2 Perturbazione tecnologica

- I micro-LED o altre tecnologie di visualizzazione potrebbero sostituire gli OLED a lungo termine.

- Se i miglioramenti in termini di costi o rendimento per Micro-LED accelerano, La crescita degli OLED potrebbe essere limitata.

12.3 Rischi commerciali e geopolitici

- Restrizioni all'esportazione, tariffe, oppure le tensioni geopolitiche potrebbero interrompere le catene di fornitura dei pannelli.

- Fare affidamento su determinate regioni per materie prime o investimenti è rischioso.

12.4 Colli di bottiglia della catena di fornitura

- Carenza di materiale organico, attrezzatura, o la manodopera qualificata potrebbe rallentare il ridimensionamento della capacità.

13. Raccomandazioni strategiche per le parti interessate

13.1 Per i produttori (Pannello)

- Investi nella capacità flessibile degli OLED e nella deposizione di nuova generazione (per esempio., getto d'inchiostro).

- Ottimizza la resa, ridurre i costi tramite l’automazione.

- Esplora le partnership per coprire i rischi (per esempio., con gli OEM, fornitori di materie prime).

13.2 Per gli OEM di smartphone

- Passare gradualmente ai modelli di fascia media verso gli OLED man mano che i costi diminuiscono.

- Utilizza OLED flessibile per dispositivi pieghevoli e fattori di forma innovativi.

- Negoziare contratti a lungo termine con i produttori di pannelli per garantire la capacità.

13.3 Per gli investitori

- Focus sui produttori di pannelli che scalano gli OLED flessibili.

- Guarda i giochi Micro-LED emergenti.

- Valutare i rischi nei progetti Fab ad alta intensità di capitale.

13.4 Per i governi & Responsabili delle politiche

- Encourage local OLED capacity via incentives.

- Support R&D in advanced display tech (OLED, MicroLED).

- Facilitate supply chain resilience (materiali, talent).

14. Future Scenarios

14.1 OLED-Dominant Scenario

- OLED becomes >70% of mobile display units by 2040.

- Flexible OLED is widespread; foldables and rollables common.

- LCD becomes niche, mostly in ultra-budget devices.

14.2 Balanced Coexistence Scenario

- OLED takes 60%+ share by 2030, but LCD remains significant (~30–40%) in lower segments.

- LCD fabs remain economically viable due to volume demand.

14.3 Disruption Scenario (MicroLED / Altro)

- Micro-LED or hybrid tech begins serious adoption in late 2030s.

- OLED growth slows; new tech eats into premium but also mid-range segments.

15. Conclusione

Over the next 20 anni, the mobile display market is likely to shift strongly toward OLED, driven by flexible form factors, falling costs, e innovazione. Tuttavia, LCD will not disappear overnight — continuerà a svolgere un ruolo importante nei segmenti sensibili ai prezzi e nei mercati emergenti. Produttori e OEM che investono saggiamente nella capacità OLED e nelle tecnologie di nuova generazione, gestendo i rischi, possono posizionarsi per beneficiare di questa trasformazione strutturale. Allo stesso tempo, le parti interessate dovrebbero prestare attenzione alle tecnologie dirompenti come Micro-LED, che potrebbe rimodellare il panorama espositivo a lungo termine.

FAQ

- Il display LCD scomparirà completamente 2045?

Non necessariamente. Mentre si prevede che l’adozione degli OLED crescerà, Gli LCD potrebbero persistere nei segmenti degli smartphone entry-level e a basso costo, soprattutto nelle regioni sensibili ai costi. - Cosa sta guidando la rapida ascesa degli OLED?

I fattori chiave includono la riduzione dei costi nella produzione di OLED, la popolarità dei telefoni pieghevoli, e le qualità di visualizzazione superiori (contrasto, flessibilità) Offerte OLED. - Quando i Micro-LED inizieranno a competere seriamente con gli OLED negli smartphone??

Il micro-LED potrebbe iniziare a sfidare l'OLED nel settore dalla fine degli anni ’30 all’inizio degli anni ’40, a seconda del costo, prodotto, e scalabilità della produzione di massa. - Esistono rischi importanti per i produttori di OLED?

Sì, i rischi includono elevate spese in conto capitale, vincoli della catena di fornitura, potenziale sconvolgimento tecnologico, e la concorrenza delle tecnologie di visualizzazione più recenti. - Quali regioni guideranno l’adozione degli OLED?

È probabile che Cina e Corea del Sud siano leader sia nella produzione che nell’adozione grazie ai forti produttori di pannelli. I mercati emergenti potrebbero seguire l’esempio man mano che i costi degli OLED diminuiranno e diventeranno flessibili / L'OLED di fascia media diventa più conveniente.