1. Введение

1.1 Purpose of the Research

This report aims to analyze and forecast the global mobile phone display panel market — specifically ЖК -дисплей (liquid crystal display) и Олинг (organic light-emitting diode) — over the next 20 годы (2025–2045). It provides insights into shipment trends, revenue growth, competitive dynamics, technological shifts, и риски, to support strategic decision-making for manufacturers, OEMs, investors, and policymakers.

1.2 Scope: Mobile LCD vs. Олинг

We focus on smartphone displays only, excluding other types such as TVs, мониторы, or automotive displays. Our analysis compares rigid and flexible OLED, different LCD variants, and projects long-term market share, technological evolution, and regional dynamics.

1.3 Methodology and Data Sources

Our forecast is based on:

- Historical data and shipment figures from Omdia (например, Omdia reports that in 2024, AMOLED shipments reached 784 миллион единиц, surpassing TFT-LCD shipments). Omdia+1

- Display revenue trends (например, SID Display Week forecast: OLED revenues $46 B in 2024, ЖК -дисплей $83 Б). Display Daily+1

- Industry research from Chinese market sources (например, Chinese OLED market projections). 中国互联网新闻网

- Market-report projections (MRFR’s smartphone display panel market from 2022 к 2032). 市场研究未来

- Additional data from corporate announcements (например, Universal Display Corp’s comments citing Omdia data). 財報狗

2. Smartphone Display Technology: An Overview

2.1 Что такое ЖК-дисплей?

ЖК -дисплей (Жидкокристаллический дисплей) is a mature display technology that uses a backlight shining through liquid crystals to create images. There are various types (TFT, IPS, и т. д.), but they all rely on a separate light source.

2.2 Что такое OLED?

Олинг (Органический светоизлучающий диод) panels emit their own light: each pixel is self-luminous. This allows deeper blacks, более высокий контраст, and potentially more power-efficient designs when parts of the screen are dark.

2.3 Ключевые различия: Власть, Гибкость, Расходы

- Власть: OLED может отключать отдельные пиксели — в некоторых случаях более энергоэффективно.

- Гибкость: OLED-панели можно сделать гибкими, включение складных телефонов.

- Расходы: Исторически, OLED стоил дороже за единицу, чем LCD, особенно для гибких или высококачественных версий.

3. Исторический контекст и эволюция рынка

3.1 Ранняя эпоха: Доминирование ЖК-дисплея

В начале 2010-х годов, ЖК-дисплей был доминирующей технологией в смартфонах из-за его более низкой стоимости и отлаженного производства.. В большинстве основных устройств используется TFT-LCD или IPS LCD..

3.2 Распространение OLED в смартфонах

За последнее десятилетие, OLED постепенно проник в смартфоны высокого класса. Преимущества контраста, форм-фактор, и энергопотребление (в темном режиме) сделал это привлекательным. Складные телефоны ускорили внедрение гибких OLED-дисплеев.

3.3 Ключевые переломные моменты

- Появление гибких OLED в складных устройствах

- Снижение затрат за счет массового производства

- Стратегические инвестиции крупных производителей панелей (например, Банк Англии, Samsung, LG)

- Transition of major OEMs to OLED for premium lines

4. Current Market Status (2024–2025 г.)

4.1 Shipment Data: OLED против ЖК-дисплея (Units)

- По данным Омдиа, в 2024, AMOLED shipments reached 784 миллион единиц, пока TFT-LCD shipments dropped to 761 миллион единиц. Omdia

- This marked the first time OLED shipments surpassed TFT-LCD in smartphones. Omdia

4.2 Revenue Landscape by Technology

- Based on the SID Display Week 2025 forecast, display revenues in 2024 were roughly: Олинг: $46 миллиард, ЖК -дисплей: $83 миллиард. Display Daily

- According to counterpoint in a translated Chinese analysis, global OLED display revenue reached доллар США 46 Б в 2024. 东方财富

- Omdia projects OLED (Амоль) revenue to reach $53 Б in the full year (future forecast). Mobile World Live

4.3 Regional Dynamics and Key Players

- Китай is a major force: Chinese OLED makers (Банк Англии, Тианма, Вижнокс, и т. д.) are scaling aggressively. Omdia+1

- Корея (Дисплей Samsung, LG) continues to play a leading role, especially in flexible OLED.

- According to a Chinese market report, flexible OLED penetration in China is expected to rise sharply; transparent/flexible technologies may also expand. 中国互联网新闻网

5. Драйверы роста OLED

5.1 Падение производственных затрат

- По мере увеличения мощности производства OLED (особенно в Китае), стоимость единицы снижается.

- Масштаб китайских производителей гибких OLED-дисплеев и конкурентоспособные цены побудили все больше OEM-производителей перейти на OLED-телефоны среднего класса.. Omdia

5.2 Гибкий / Тренд складных смартфонов

- Рост популярности складных телефонов стимулирует спрос на гибкие OLED.

- Согласно отчетам китайской промышленности, складные форм-факторы являются основным фактором будущего внедрения OLED. 中国互联网新闻网

5.3 Энергоэффективность & Опыт показа

- Способность OLED отключать пиксели обеспечивает экономию энергии, особенно в темных режимах пользовательского интерфейса.

- Пользователи все чаще требуют более насыщенных визуальных эффектов, высокая частота обновления, и гибкие форм-факторы.

5.4 Инновации в материалах и технологиях

- Новые процессы, такие как OLED с струйной печатью и экономичное осаждение повышают производительность и сокращают затраты.

- Gen-8.6 и другие передовые заводы строятся для расширения производства.. Omdia

6. Проблемы внедрения OLED

6.1 Давление на производственные затраты

Производство OLED (особенно гибкий) остается более сложным и дорогим, чем ЖК-дисплей. Масштабирование требует капиталоемких производств.

6.2 Конкуренция со стороны новых технологий

- Микро-светодиод: Хотя все еще появляется, Микросветодиоды представляют собой потенциальную долгосрочную угрозу.

- QD OLED: Комбинированные технологии могут конкурировать в премиальном сегменте.

6.3 Риски цепочки поставок

Сырье (органические соединения, герметизирующие материалы) и специализированное оборудование может стать узким местом производства.

6.4 Риск выгорания & Долголетие

OLED-панели могут выгорать при определенных условиях., вызывает обеспокоенность по поводу долгосрочной надежности у некоторых пользователей.

7. Роль ЖК-дисплеев в будущем

7.1 Почему ЖК-дисплей остается актуальным

- Более дешевое производство

- Уже существующие крупные мощности

- Более простая и стабильная цепочка поставок

7.2 Бюджетный / Сегмент бюджетных смартфонов

Для телефонов начального уровня и ниже среднего., ЖК-дисплеи могут оставаться доминирующими из-за своего ценового преимущества..

7.3 LCD Production Capacity Trends

Some LCD fabs are being repurposed, but many remain active for mobile display production.

7.4 Regionally Differentiated Demand

In markets where cost sensitivity is high (emerging markets), LCD will likely still serve a large portion of demand.

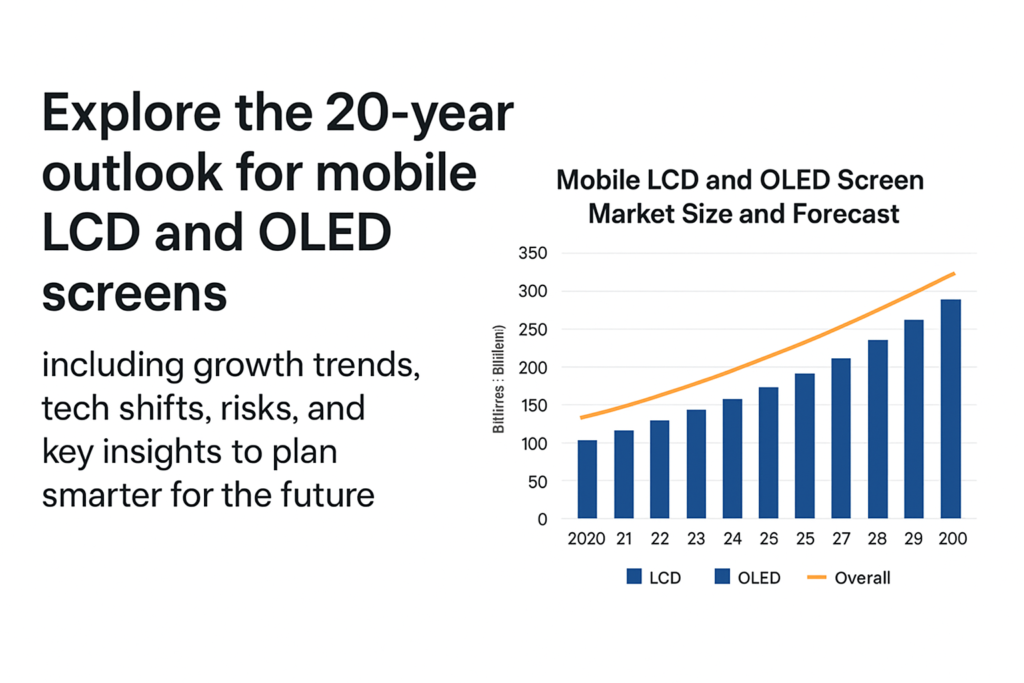

8. Market Size Forecast (2025–2045)

8.1 Base-case Scenario Assumptions

- Continued OLED adoption, особенно гибкий

- Moderate decline in LCD units but stable for budget segment

- No sudden disruption from Micro-LED before 2035

8.2 OLED Shipment Forecast

- Олинг (Амоль) shipments: growing from ~0.78 B in 2024, to over 1.2–1.4B units annually by the early 2030s (projected estimate based on trend)

- Revenue growth: from ~$46B in 2024 to potentially ~$70B+ in peak years (assuming ASPs stabilize or slightly drop but volume increases)

8.3 LCD Shipment Forecast

- Поставки ЖК-дисплеев могут снизиться в абсолютных единицах, например, от 761 М в 2024, постепенно, возможно, 400–600 М в последующие годы, когда OLED заполнит верхний/средний сегменты

- Доход: снижение отражает как снижение количества единиц продукции, так и ценовое давление; но все же значительная часть общего рынка мобильных дисплеев приходится на устройства более низкого уровня..

8.4 Доля OLED и LCD с течением времени

- К 2030, OLED может захватывать 60–70%+ рынка дисплеев для смартфонов по единицам (тем более, что гибкий подход становится все более распространенным)

- К 2040, возможно, мы увидим OLED доминирующий (>70%) если новый сбой не ускорится.

9. Технологические тенденции & Инновации

9.1 Гибкий и складной OLED

- Складные телефоны будут продолжать стимулировать спрос на гибкие OLED-экраны.

- Больше OEM-производителей могут выпустить сворачиваемые или растягивающиеся устройства, растущий спрос на гибкие панели.

9.2 ЛТПО, Тандемный OLED, Струйная печать

- ЛТПО (Низкотемпературный поликристаллический оксид) backplanes enable variable refresh rates and power savings.

- Тандемный OLED stacks layers to extend lifetime and reduce power.

- Inkjet-printed OLED can potentially lower manufacturing costs and increase yield.

9.3 Hybrid Technologies

- QD OLED (quantum dot + Олинг) might target premium markets.

- Микро-светодиод: while still nascent, medium-term growth (post-2030) could challenge OLED in some segments.

9.4 Sustainability & Энергоэффективность

- OLED’s energy savings in dark UIs help for power efficiency.

- Manufacturers may invest more in eco-friendly materials and recycling.

10. Regional Market Forecast

10.1 Китай

- Strong OLED capacity build-out.

- Massive domestic smartphone production and adoption.

- Flexible OLED is already being scaled by Chinese makers.

10.2 Южная Корея

- Home to Samsung Display and LG, continuing high-end flexible OLED leadership.

- Likely to remain key in innovation.

10.3 Европа & Северная Америка

- Premium device segments.

- Stable demand, но чувствительность к цене может замедлить полное проникновение OLED в средний диапазон.

10.4 Развивающиеся рынки (Индия, Юго-Восточная Азия)

- Чувствителен к цене: ЖК-дисплей может продолжать оставаться сильным здесь.

- Но поскольку стоимость OLED падает, OLED среднего класса может стать мейнстримом.

11. Конкурентная среда & Ключевые игроки

11.1 Основные производители OLED-панелей

- Дисплей Samsung: сильный в области гибких и премиальных OLED.

- LG Дисплей: Олинг, гибкий, но более ограничен в небольших мобильных устройствах.

- Банк Англии / Вижнокс / Тианма (Китай): быстро растет, конкурентоспособный по стоимости.

11.2 Производители ЖК-панелей & Их стратегия

- Некоторые производители ЖК-дисплеев сокращают размеры; другие могут перейти на нишевые или специализированные ЖК-дисплеи..

- Производители устаревших ЖК-дисплеев должны решить, инвестировать ли в OLED или модернизировать.

11.3 Новые участники / Прорывные игроки

- Новые производители микросветодиодов.

- Стартапы, работающие над OLED-процессами нового поколения (например, струйный, тандем).

12. Риски и неопределенности

12.1 Макроэкономические риски

- Рецессии, инфляция, Потрясения в цепочке поставок могут замедлить спрос на смартфоны.

- Капиталоемкость новых фабрик высока — риск, если спрос замедлится.

12.2 Технологический прорыв

- Micro-LED or other display technologies could displace OLED in the long term.

- If cost or yield improvements for Micro-LED accelerate, OLED’s growth could be capped.

12.3 Trade and Geopolitical Risks

- Export restrictions, тарифы, or geopolitical tensions could disrupt panel supply chains.

- Reliance on particular regions for raw materials or investments is risky.

12.4 Supply Chain Bottlenecks

- Shortage of organic material, оборудование, or skilled labor could slow capacity scaling.

13. Strategic Recommendations for Stakeholders

13.1 Для производителей (Панель)

- Invest in flexible OLED capacity and next-gen deposition (например, струйный).

- Optimize yield, reduce cost via automation.

- Explore partnerships to hedge risks (например, with OEMs, raw material suppliers).

13.2 For Smartphone OEMs

- Gradually shift mid-range models to OLED as costs drop.

- Use flexible OLED for foldables and innovative form factors.

- Negotiate long-term contracts with panel makers to secure capacity.

13.3 Для инвесторов

- Focus on panel makers scaling flexible OLED.

- Watch for emerging Micro-LED plays.

- Assess risks in capital-intensive fab projects.

13.4 For Governments & Policy Makers

- Encourage local OLED capacity via incentives.

- Support R&D in advanced display tech (Олинг, Микро-светодиод).

- Facilitate supply chain resilience (материалы, talent).

14. Future Scenarios

14.1 OLED-Dominant Scenario

- OLED becomes >70% of mobile display units by 2040.

- Flexible OLED is widespread; foldables and rollables common.

- LCD becomes niche, mostly in ultra-budget devices.

14.2 Balanced Coexistence Scenario

- OLED takes 60%+ share by 2030, but LCD remains significant (~30–40%) in lower segments.

- LCD fabs remain economically viable due to volume demand.

14.3 Disruption Scenario (Микро-светодиод / Другой)

- Micro-LED or hybrid tech begins serious adoption in late 2030s.

- OLED growth slows; new tech eats into premium but also mid-range segments.

15. Заключение

Over the next 20 годы, the mobile display market is likely to shift strongly toward OLED, driven by flexible form factors, falling costs, и инновации. Однако, LCD will not disappear overnight — it will continue to play an important role in price-sensitive segments and emerging markets. Manufacturers and OEMs who invest wisely in OLED capacity and next-gen technologies, while managing risks, can position themselves to benefit from this structural transformation. В то же время, stakeholders should watch for disruptive technologies like Micro-LED, which could reshape the display landscape in the long run.

Часто задаваемые вопросы

- Will LCD completely disappear by 2045?

Не обязательно. While OLED adoption is expected to grow, LCD may persist in low-cost and entry-level smartphone segments, especially in cost-sensitive regions. - What is driving the rapid rise of OLED?

Key drivers include cost reductions in OLED manufacturing, the popularity of foldable phones, and the superior display qualities (контраст, гибкость) OLED offers. - When might Micro-LED start to seriously compete with OLED in smartphones?

Micro-LED may begin to challenge OLED in the late 2030s to early 2040s, depending on cost, yield, and mass production scalability. - Are there major risks for OLED manufacturers?

Yes — risks include high capital expenditure, supply chain constraints, potential technological disruption, and competition from newer display technologies. - Which regions will lead OLED adoption?

China and South Korea are likely to lead in both production and adoption due to strong panel makers. Emerging markets may follow as OLED costs drop and flexible / mid-range OLED becomes more affordable.