1. Invoering

1.1 Doel van het onderzoek

Dit rapport is bedoeld om specifiek de wereldwijde markt voor displaypanelen voor mobiele telefoons te analyseren en te voorspellen LCD (LCD-scherm) En OLED (organische lichtgevende diode) — boven de volgende 20 jaar (2025–2045). Het biedt inzicht in verzendtrends, omzetgroei, concurrentiedynamiek, technologische verschuivingen, en risico's, ter ondersteuning van strategische besluitvorming voor fabrikanten, OEM's, investeerders, en beleidsmakers.

1.2 Domein: Mobiel LCD-scherm vs. OLED

Wij concentreren ons op alleen smartphone-displays, met uitzondering van andere typen zoals tv's, monitoren, of autodisplays. Onze analyse vergelijkt stijve en flexibele OLED, verschillende LCD-varianten, en projecteert marktaandeel op lange termijn, technologische evolutie, en regionale dynamiek.

1.3 Methodologie en gegevensbronnen

Onze voorspelling is gebaseerd op:

- Historische gegevens en verzendcijfers van Omdia (bijv., Dat meldt Omdia 2024, AMOLED-zendingen bereikt 784 miljoen eenheden, overtreft TFT-LCD-zendingen). Omdia+1

- Geef omzettrends weer (bijv., SID Weergaveweekvoorspelling: OLED-inkomsten $46 B-in 2024, LCD $83 B). Dagelijks+1 weergeven

- Industrieonderzoek uit bronnen op de Chinese markt (bijv., Chinese OLED-marktprojecties). China internetnieuwsnetwerk

- Marktrapportprojecties (MRFR's smartphone-displaypaneelmarkt van 2022 naar 2032). marktonderzoek toekomst

- Aanvullende gegevens uit bedrijfsaankondigingen (bijv., De opmerkingen van Universal Display Corp onder verwijzing naar Omdia-gegevens). financieel rapport hond

2. Smartphone-weergavetechnologie: Een overzicht

2.1 Wat is LCD?

LCD (Vloeibare kristalweergave) is een volwassen weergavetechnologie die gebruikmaakt van achtergrondverlichting die door vloeibare kristallen schijnt om afbeeldingen te creëren. Er zijn verschillende soorten (Tft, IPS, enz.), maar ze zijn allemaal afhankelijk van een afzonderlijke lichtbron.

2.2 Wat is OLED?

OLED (Organische lichtemitterende diode) panelen stralen hun eigen licht uit: elke pixel is zelflichtgevend. Dit maakt diepere zwarttinten mogelijk, hoger contrast, en potentieel energiezuinigere ontwerpen wanneer delen van het scherm donker zijn.

2.3 Belangrijkste verschillen: Stroom, Flexibiliteit, Kosten

- Stroom: OLED kan individuele pixels uitschakelen, wat in sommige gevallen energiezuiniger is.

- Flexibiliteit: OLED-panelen kunnen flexibel gemaakt worden, waardoor opvouwbare telefoons mogelijk worden.

- Kosten: Historisch gezien, OLED is per eenheid duurder geweest dan LCD, vooral voor flexibele of high-end versies.

3. Historische context en marktevolutie

3.1 Vroeg tijdperk: Dominantie van LCD

Begin 2010, LCD was de dominante technologie in smartphones vanwege de lagere kosten en volwassen productie. De meeste reguliere apparaten gebruikten TFT-LCD of IPS LCD.

3.2 Opkomst van OLED in smartphones

Het afgelopen decennium, OLED infiltreerde geleidelijk in de high-end smartphones. De voordelen van contrast, vormfactor, en energieverbruik (in de donkere modus) maakte het aantrekkelijk. Opvouwbare telefoons versnelden de flexibele adoptie van OLED.

3.3 Belangrijke buigpunten

- Invoer van flexibele OLED in opvouwbare producten

- Kostenreductie door massaproductie

- Strategische investeringen door grote paneelmakers (bijv., BOE, Samsung, LG)

- Overgang van grote OEM's naar OLED voor premiumlijnen

4. Huidige marktstatus (2024–2025)

4.1 Verzendingsgegevens: OLED versus LCD (Eenheden)

- Volgens Omdia, in 2024, AMOLED-zendingen bereikt 784 miljoen eenheden, terwijl TFT-LCD-zendingen gedaald naar 761 miljoen eenheden. Omdia

- Dit markeerde de eerste keer OLED-leveringen overtroffen TFT-LCD in smartphones. Omdia

4.2 Inkomstenlandschap per technologie

- Gebaseerd op de SID Display Week 2025 voorspelling, omzet weergeven 2024 waren ongeveer: OLED: $46 miljard, LCD: $83 miljard. Dagelijks weergeven

- Volgens contrapunt in een vertaalde Chinese analyse, De wereldwijde omzet uit OLED-displays is bereikt USD 46 B in 2024. Oosters fortuin

- Omdia projecteert OLED (AMOLED) omzet te bereiken $53 B in het volledige jaar (toekomstige voorspelling). Mobiele wereld live

4.3 Regionale dynamiek en sleutelspelers

- China is een grote kracht: Chinese OLED-makers (BOE, Tianma, Visiox, enz.) zijn agressief aan het schalen. Omdia+1

- Korea (Samsung-scherm, LG) blijft een leidende rol spelen, vooral in flexibele OLED.

- Dat blijkt uit een Chinees marktrapport, De verwachting is dat de flexibele OLED-penetratie in China sterk zal stijgen; transparante/flexibele technologieën kunnen zich ook uitbreiden. China internetnieuwsnetwerk

5. Aanjagers van OLED-groei

5.1 Dalende productiekosten

- Naarmate de OLED-fabriekscapaciteit toeneemt (vooral in China), de kosten per eenheid dalen.

- De schaal van de Chinese flexibele OLED-fabrikant en concurrerende prijzen zorgden ervoor dat meer OEM's overgingen op telefoons uit het middensegment naar OLED. Omdia

5.2 Flexibele / Opvouwbare smartphonetrend

- De opkomst van opvouwbare telefoons stimuleert de vraag naar flexibele OLED.

- Dat blijkt uit rapporten uit de Chinese industrie, Opvouwbare vormfactoren zijn een belangrijke motor voor de toekomstige adoptie van OLED. China internetnieuwsnetwerk

5.3 Energie-efficiëntie & Ervaring weergeven

- Het vermogen van OLED om pixels uit te schakelen, biedt energiebesparingen, vooral in donkere UI-modi.

- Gebruikers eisen steeds rijkere beelden, Hoge verversingspercentages, en flexibele vormfactoren.

5.4 Innovatie in materialen en fabrieken

- Nieuwe processen zoals inkjet-geprinte OLED en kostenefficiënte depositie verbeteren de opbrengst en verlagen de kosten.

- Gen-8.6 en andere geavanceerde fabrieken worden gebouwd om de productie op te schalen. Omdia

6. Uitdagingen voor OLED-adoptie

6.1 Druk op de productiekosten

OLED-productie (bijzonder flexibel) blijft complexer en duurder dan LCD. Voor schaalvergroting zijn kapitaalintensieve fabrieken nodig.

6.2 Concurrentie van opkomende technologieën

- Micro-LED: Hoewel het nog steeds in opkomst is, Micro-LED is een potentiële bedreiging op de lange termijn.

- QD OLED: Combinatietechnologieën kunnen concurreren in premiumsegmenten.

6.3 Risico's voor de toeleveringsketen

Grondstoffen (organische verbindingen, inkapselingsmaterialen) en gespecialiseerde apparatuur kan de productie belemmeren.

6.4 Risico op inbranden & Levensduur

OLED-panelen kunnen onder bepaalde omstandigheden inbranden, Dit roept bij sommige gebruikers zorgen op over de betrouwbaarheid op lange termijn.

7. De rol van LCD in de toekomst

7.1 Waarom LCD relevant blijft

- Goedkopere productie

- Er bestaat al capaciteit voor grote volumes

- Een eenvoudigere en stabielere toeleveringsketen

7.2 Lage kosten / Budgetsmartphonesegment

For entry-level and lower mid-range phones, LCD may remain dominant because of its cost advantage.

7.3 LCD Production Capacity Trends

Some LCD fabs are being repurposed, but many remain active for mobile display production.

7.4 Regionally Differentiated Demand

In markets where cost sensitivity is high (emerging markets), LCD will likely still serve a large portion of demand.

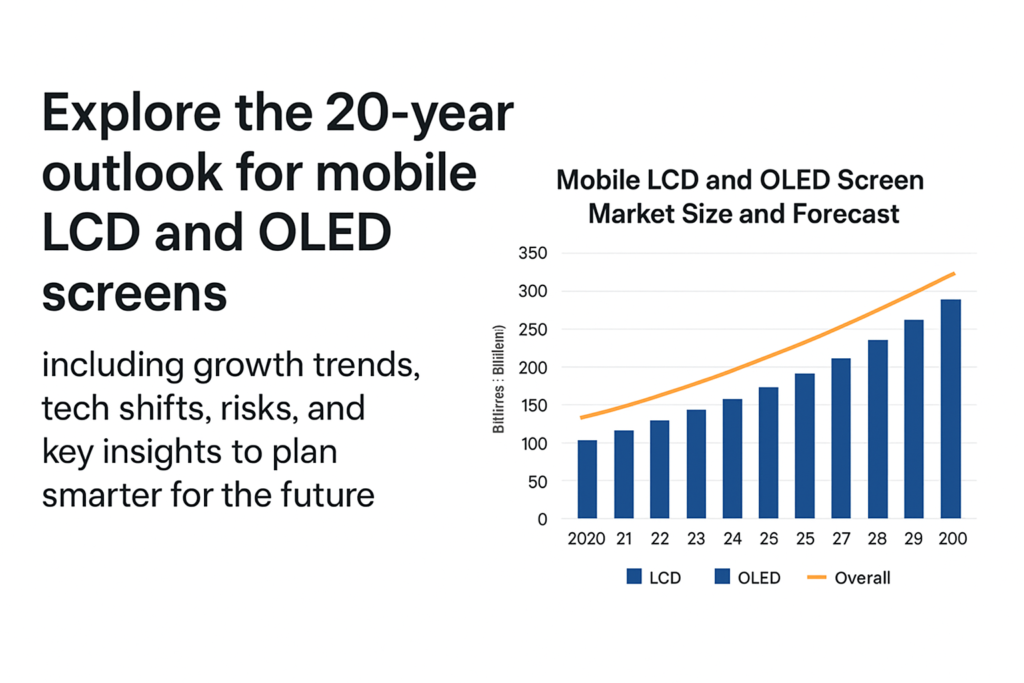

8. Market Size Forecast (2025–2045)

8.1 Base-case Scenario Assumptions

- Continued OLED adoption, bijzonder flexibel

- Moderate decline in LCD units but stable for budget segment

- No sudden disruption from Micro-LED before 2035

8.2 OLED Shipment Forecast

- OLED (AMOLED) shipments: growing from ~0.78 B in 2024, to over 1.2–1.4B units annually by the early 2030s (projected estimate based on trend)

- Revenue growth: from ~$46B in 2024 to potentially ~$70B+ in peak years (assuming ASPs stabilize or slightly drop but volume increases)

8.3 LCD Shipment Forecast

- LCD-verzendingen kunnen in absolute eenheden afnemen, b.v., van 761 M in 2024, geleidelijk aan misschien 400–600 M in latere jaren, aangezien OLED de hoge/middensegmenten vult

- Winst: De daling weerspiegelt zowel lagere eenheden als prijsdruk; maar nog steeds een aanzienlijk deel van de totale mobiele displaymarkt vanwege het volume op lagere apparaten.

8.4 OLED versus LCD-aandeel in de loop van de tijd

- Door 2030, OLED zou kunnen vastleggen 60–70%+ van de markt voor smartphonedisplays per eenheid (vooral omdat flexibel steeds gebruikelijker wordt)

- Door 2040, het is mogelijk dat we OLED zien bestaan dominant (>70%) tenzij een nieuwe verstoring zich versnelt.

9. Technologische trends & Innovaties

9.1 Flexibel en opvouwbaar OLED

- Opvouwbare telefoons zullen de vraag naar flexibele OLED blijven stimuleren.

- Meer OEM's zullen mogelijk oprolbare of rekbare apparaten lanceren, toenemende vraag naar flexibele panelen.

9.2 LTPO, Tandem-OLED, Inkjetafdrukken

- LTPO (Polykristallijn oxide bij lage temperatuur) backplanes maken variabele vernieuwingsfrequenties en energiebesparingen mogelijk.

- Tandem-OLED stapelt lagen om de levensduur te verlengen en het vermogen te verminderen.

- Inkjet-geprinte OLED kan mogelijk de productiekosten verlagen en de opbrengst verhogen.

9.3 Hybride technologieën

- QD OLED (kwantum punt + OLED) zouden zich kunnen richten op premiummarkten.

- Micro-LED: terwijl het nog in de kinderschoenen staat, groei op de middellange termijn (na 2030) zou OLED in sommige segmenten kunnen uitdagen.

9.4 Duurzaamheid & Energie-efficiëntie

- De energiebesparingen van OLED in donkere gebruikersinterfaces dragen bij aan de energie-efficiëntie.

- Fabrikanten kunnen meer investeren in milieuvriendelijke materialen en recycling.

10. Regionale marktvoorspelling

10.1 China

- Sterke OLED-capaciteitsopbouw.

- Enorme binnenlandse productie en adoptie van smartphones.

- Flexibele OLED wordt al opgeschaald door Chinese makers.

10.2 Zuid-Korea

- Thuisbasis van Samsung Display en LG, aanhoudend high-end flexibel OLED-leiderschap.

- Zal waarschijnlijk de sleutel blijven tot innovatie.

10.3 Europa & Noord-Amerika

- Premium apparaatsegmenten.

- Stabiele vraag, maar de kostengevoeligheid kan de volledige OLED-penetratie in het middensegment vertragen.

10.4 Opkomende markten (India, Zuidoost-Azië)

- Prijsgevoelig: LCD kan hier sterk blijven.

- Maar naarmate de OLED-kosten dalen, OLED uit het middensegment kan mainstream worden.

11. Competitief landschap & Belangrijkste spelers

11.1 Grote fabrikanten van OLED-panelen

- Samsung-scherm: sterk in flexibele en premium OLED.

- LG-scherm: OLED, flexibele, maar beperkter in kleine mobieltjes.

- BOE / Visiox / Tianma (China): groeit snel, kostenconcurrerend.

11.2 Fabrikanten van LCD-panelen & Hun strategie

- Sommige LCD-fabrikanten zijn aan het inkrimpen; anderen kunnen zich richten op niche- of speciale LCD-schermen.

- Oudere LCD-makers moeten beslissen of ze in OLED willen investeren of dat ze willen stroomlijnen.

11.3 Nieuwe deelnemers / Disruptieve spelers

- Opkomende micro-LED-fabrikanten.

- Startups die werken aan OLED-processen van de volgende generatie (bijv., inkjet, tandem).

12. Risico's en onzekerheden

12.1 Macro-economische risico's

- recessies, inflatie, Schokken in de toeleveringsketen kunnen de vraag naar smartphones vertragen.

- De kapitaalintensiteit van nieuwe fabrieken is hoog – risico als de vraag vertraagt.

12.2 Technologische disruptie

- Micro-LED of andere weergavetechnologieën kunnen OLED op de lange termijn vervangen.

- Als de kosten- of opbrengstverbeteringen voor Micro-LED versnellen, De groei van OLED zou kunnen worden afgetopt.

12.3 Handels- en geopolitieke risico's

- Exportbeperkingen, tarieven, of geopolitieke spanningen kunnen de toeleveringsketens van panelen ontwrichten.

- Afhankelijkheid van bepaalde regio's voor grondstoffen of investeringen is riskant.

12.4 Knelpunten in de toeleveringsketen

- Tekort aan organisch materiaal, apparatuur, of geschoolde arbeidskrachten zouden de schaalvergroting van de capaciteit kunnen vertragen.

13. Strategische aanbevelingen voor belanghebbenden

13.1 Voor fabrikanten (Paneel)

- Investeer in flexibele OLED-capaciteit en depositie van de volgende generatie (bijv., inkjet).

- Optimaliseer de opbrengst, kosten verlagen via automatisering.

- Ontdek partnerschappen om risico's af te dekken (bijv., met OEM's, leveranciers van grondstoffen).

13.2 Voor smartphone-OEM's

- Stap geleidelijk over op OLED-modellen uit het middensegment naarmate de kosten dalen.

- Gebruik flexibele OLED voor opvouwbare producten en innovatieve vormfactoren.

- Negotiate long-term contracts with panel makers to secure capacity.

13.3 Voor investeerders

- Focus on panel makers scaling flexible OLED.

- Watch for emerging Micro-LED plays.

- Assess risks in capital-intensive fab projects.

13.4 For Governments & Policy Makers

- Encourage local OLED capacity via incentives.

- Support R&D in advanced display tech (OLED, Micro-LED).

- Facilitate supply chain resilience (materialen, talent).

14. Future Scenarios

14.1 OLED-Dominant Scenario

- OLED becomes >70% of mobile display units by 2040.

- Flexible OLED is widespread; foldables and rollables common.

- LCD becomes niche, mostly in ultra-budget devices.

14.2 Balanced Coexistence Scenario

- OLED takes 60%+ share by 2030, but LCD remains significant (~30–40%) in lower segments.

- LCD fabs remain economically viable due to volume demand.

14.3 Disruption Scenario (Micro-LED / Ander)

- Micro-LED or hybrid tech begins serious adoption in late 2030s.

- OLED growth slows; new tech eats into premium but also mid-range segments.

15. Conclusie

Over de volgende 20 jaar, de markt voor mobiele displays zal dat waarschijnlijk ook doen sterk verschuiven naar OLED, gedreven door flexibele vormfactoren, dalende kosten, en innovatie. Echter, LCD zal niet van de ene op de andere dag verdwijnen — het zal een belangrijke rol blijven spelen in prijsgevoelige segmenten en opkomende markten. Fabrikanten en OEM's die verstandig investeren in OLED-capaciteit en technologieën van de volgende generatie, terwijl u de risico's beheert, kunnen zichzelf positioneren om te profiteren van deze structurele transformatie. Tegelijkertijd, belanghebbenden moeten uitkijken naar disruptieve technologieën zoals Micro-LED, die op de lange termijn het displaylandschap opnieuw vorm zouden kunnen geven.

FAQ's

- Zal LCD volledig verdwijnen? 2045?

Niet noodzakelijkerwijs. Terwijl de adoptie van OLED naar verwachting zal groeien, LCD kan blijven bestaan in goedkope en instapsmartphonesegmenten, vooral in kostengevoelige regio's. - Wat is de drijvende kracht achter de snelle opkomst van OLED??

Belangrijke drijfveren zijn onder meer kostenbesparingen bij de OLED-productie, de populariteit van opvouwbare telefoons, en de superieure weergavekwaliteiten (contrast, flexibiliteit) OLED-aanbiedingen. - Wanneer zou Micro-LED serieus kunnen gaan concurreren met OLED in smartphones??

Micro-LED kan OLED gaan uitdagen in de toekomst eind 2030 tot begin 2040, afhankelijk van de kosten, opbrengst, en schaalbaarheid van massaproductie. - Zijn er grote risico’s voor OLED-fabrikanten??

Ja – risico's omvatten hoge kapitaaluitgaven, beperkingen van de toeleveringsketen, potentiële technologische disruptie, en concurrentie van nieuwere displaytechnologieën. - Welke regio's zullen de adoptie van OLED leiden?

China en Zuid-Korea zullen waarschijnlijk het voortouw nemen in zowel de productie als de adoptie dankzij de sterke paneelfabrikanten. Opkomende markten kunnen volgen naarmate de OLED-kosten dalen en flexibeler worden / OLED uit het middensegment wordt betaalbaarder.